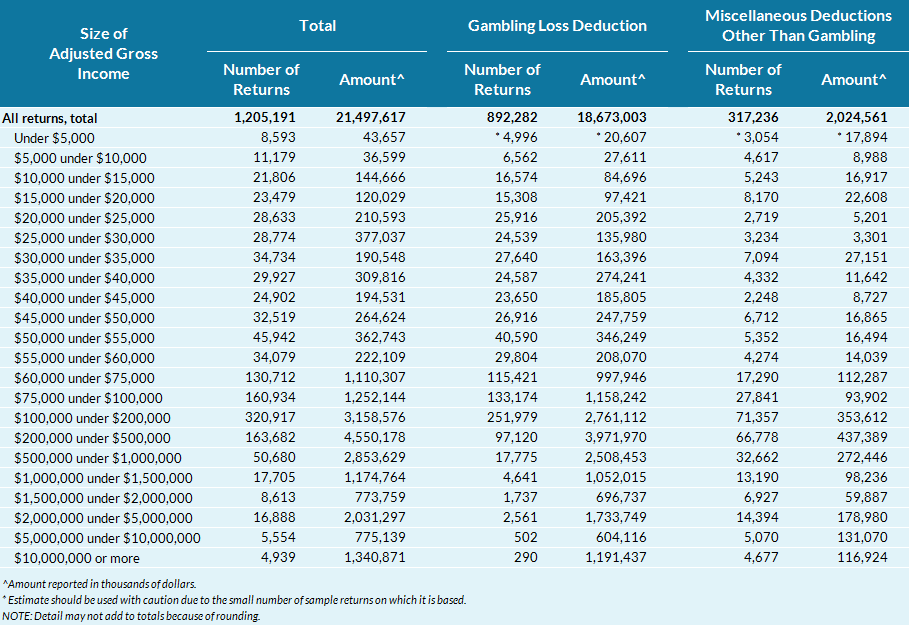

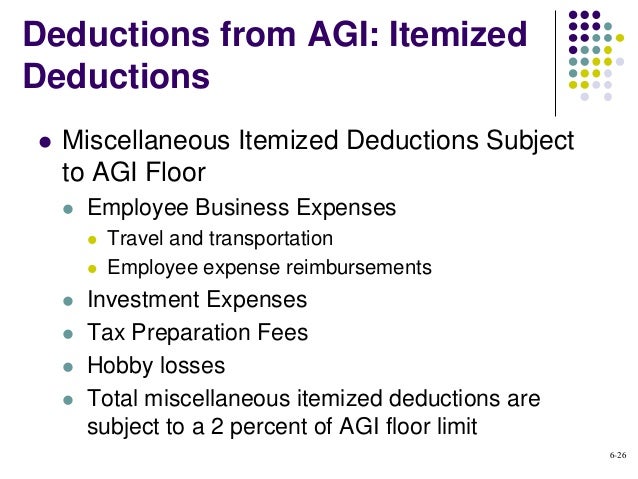

Miscellaneous Itemized Deductions Floor

The Ultimate List Of Itemized Deductions Standard Deduction Deduction Tax Deductions List

Tax Deductions Above The Line Standard Itemized And Miscellaneous

It Is Such A Shame To Work All Year Find Out You Have Money Coming Back And Th Tax Day Tax Forms Tax Time

It S Your Favorite Post Of The Week Time To Test Your Knowledge With An Mcq Leave A Comment With Your Answer And We Ll Let Yaeger Cpa Review Blog Cpa R

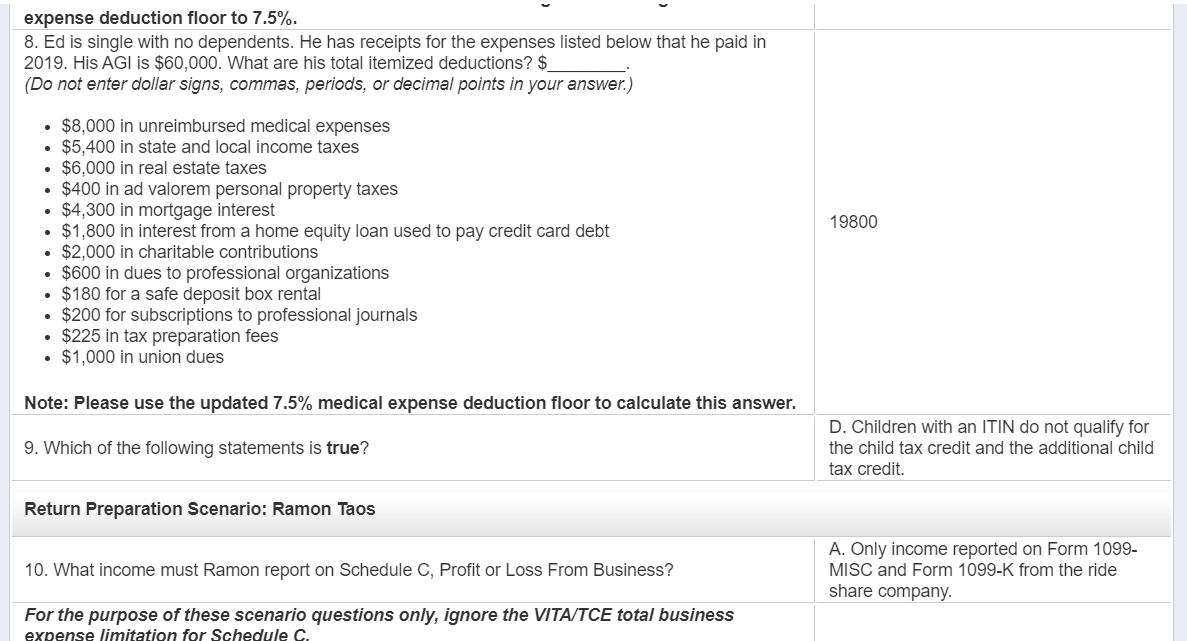

Expense Deduction Floor To 7 5 8 Ed Is Single W Chegg Com

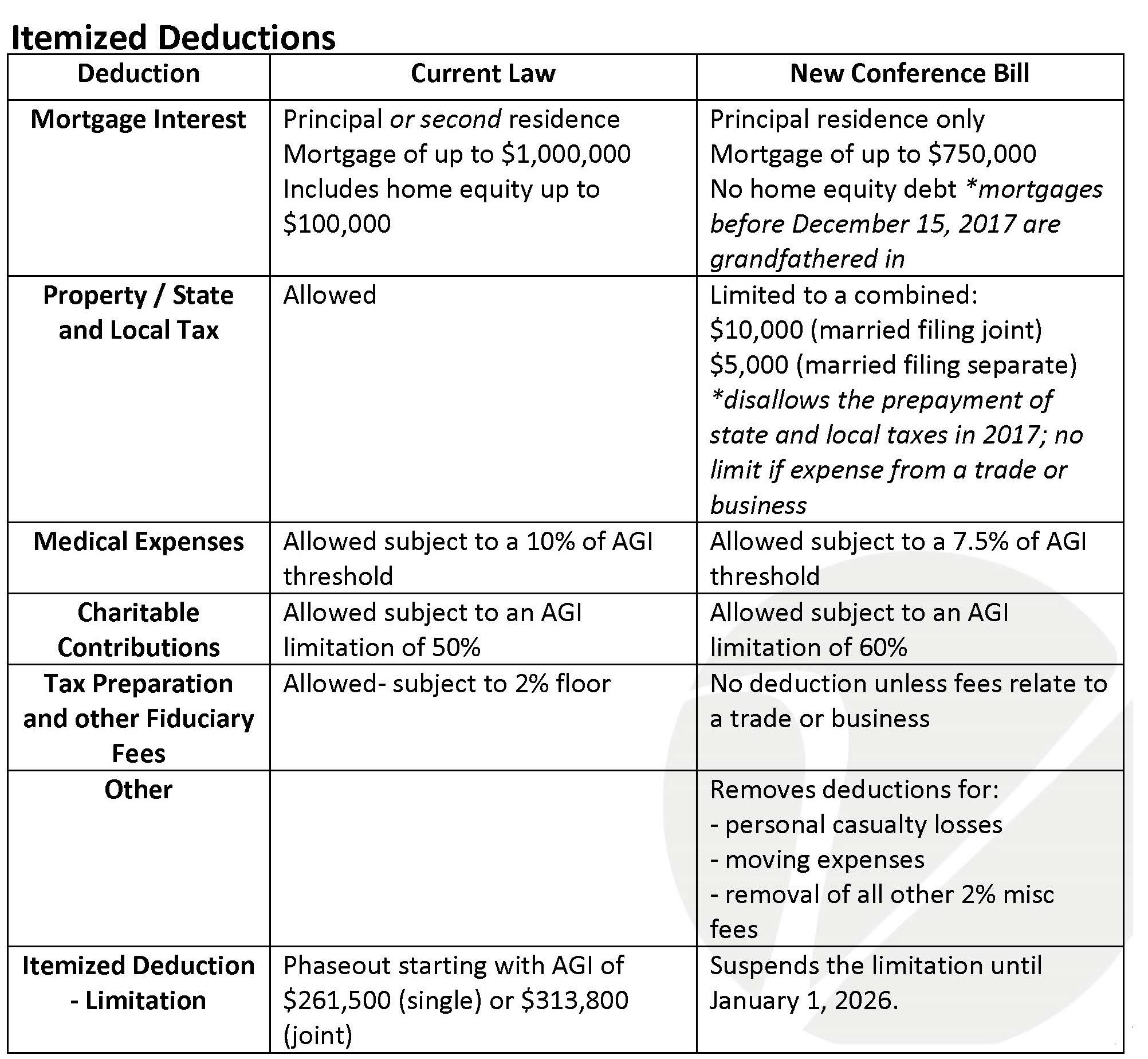

Tax Reform 2018 The Impact On Itemized Deductions For Individuals Jfs Wealth Advisors

Deductible expenses subject to the 2 floor includes.

Miscellaneous itemized deductions floor.

Known Facts About Direct Admission In Top Mba College University Of Delhi College Names Mba

Keep Your Agency Profitable And Compliant With The Coding Institute S Post Acute Newsletters To Avail Additional 20 O Medical Coding Post Acute Care Coding

6980905 The European Union Reform Company

Investment Fees Are Not Deductible But Borrow Fees Are Investing Best Term Life Insurance Life Insurance Companies

Key Retirement And Tax Numbers For 2018 Alexandria Capital

Pin On Lapsesad

How To Deduct Mortgage Points On Your Tax Return Turbotax Tax Tips Videos Buying A New Home Moving House Home Buying

Quick Guide To Xat 2020 Mba Entrance Exam Direct Admission With Images Entrance Exam Mba Admissions

Can You Deduct Home Office Expenses Emil Estafanous Cpa Cff Cgma Home Office Space Home Office Expenses Space Interiors

Www Hcpro Com Coding Medical Coder Similarities And Differences

Toughest Examsin The World How To Memorize Things Mba Admissions

Reminder To Renter Of Missed Rent Payment Http Gtldworldcongress Com Free Rental Agreement Fo Being A Landlord Property Management Rental Agreement Templates

My Slideshow Healthcare Jobs Career Development Solutions

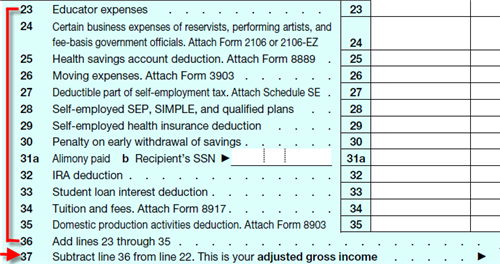

Interactive Tax Forms

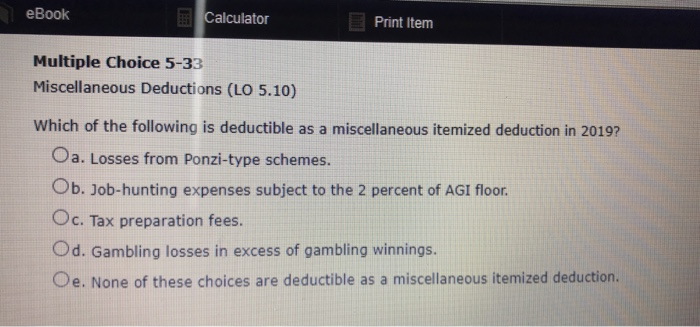

Solved Ebook Calculator Print Item Multiple Choice 5 33 M Chegg Com

Acct321 Chapter 06

Tax Reform At A Glance How Does It Affect You

Benefits Of The House Tax Cuts And Jobs Act

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcsbrmabmhloqccxoh0vzdwtaefjqpyf9 Etoelsib1w1pu3qeqj Usqp Cau

Payroll Specialist Perfect Xmas Gift T Shirt Shirts Mens Tshirts

You Can Get Away With Your Black Money Life Insurance Companies

Payroll Specialist Perfect Xmas Gift T Shirt Shirts Mens Tshirts

Pin On Supercoder S Videos

Non Renewal Notice Ez Landlord Forms Http Gtldworldcongress Com Free Rental Agreement Form Being A Landlord Lease Agreement Tenancy Agreement

Source : pinterest.com